Crypto ATM Safety Checker

Use this tool to evaluate whether a crypto ATM is likely to be safe or potentially fraudulent. Answer the following questions based on your experience or observations.

Your assessment will appear here after clicking "Check Safety Score"

In 2024 alone, fraudsters ripped off victims of more than crypto ATM scams for a jaw‑dropping $246.7million. Those numbers aren’t a fluke - they’re the tip of an iceberg that’s growing faster than the machines themselves. If you’ve ever thought about walking up to a kiosk, dropping cash in, and walking out with Bitcoin, you need to know what’s really happening behind the screen.

What Exactly Is a Crypto ATM?

When you see a cryptocurrency ATM is a kiosk that lets you exchange fiat cash for digital assets like Bitcoin, Ethereum, or stablecoins and vice versa, you’re dealing with a device that promises instant access to the blockchain. Most models accept cash, debit cards, or QR codes, then dispense a paper receipt with a wallet address. The appeal is obvious: no bank account, no lengthy verification, just a quick buy or sell.

How Big Is the Fraud Problem?

The FBI’s Internet Crime Complaint Center (IC3) logged 10,956 complaints about crypto ATMs in 2024, translating to the $246.7million loss figure cited by law‑enforcement officials. Even scarier, two‑thirds of those victims were over 60years old, a demographic that saw a 99% jump in complaints compared with previous years. States like Arizona are feeling the heat - residents there reported $177million in losses, with Scottsdale alone losing $5million this year.

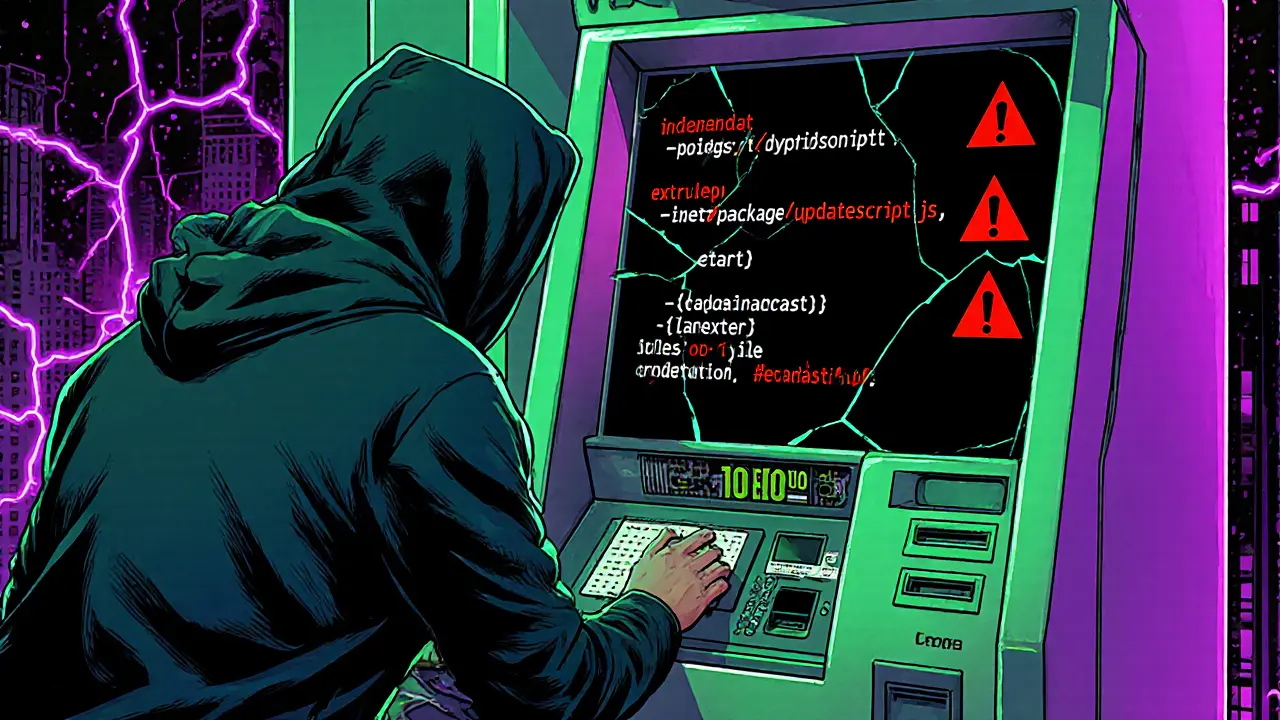

Technical Vulnerabilities: The Lamassu Case Study

Not all crypto ATMs are created equal. Security researcher Gabriel Gonzalez from IOActive uncovered three critical bugs in the Lamassu Douro Bitcoin ATM - CVE‑2024‑0674, CVE‑2024‑0675, and CVE‑2024‑0676. The worst, CVE‑2024‑0674, lets an attacker drop a malicious file at /tmp/extract/package/updatescript.js and gain root access during an update, essentially turning the machine into a hacker’s playground.

These flaws affect the Douro model from Lamassu Industries AG - a company that supplies over 1,200 crypto ATMs worldwide - and similar issues may linger in newer firmware versions.

Regulatory Gaps vs. Traditional ATMs

Traditional bank ATMs operate under a web of federal rules: the Bank Secrecy Act (BSA), anti‑money‑laundering (AML) checks, transaction monitoring, and mandatory reporting of suspicious activity. Crypto ATMs, by contrast, often slip through those nets. The National Consumers League calls them “largely unregulated,” and many operators skip BSA obligations altogether.

Arizona’s new Cryptocurrency Kiosk License Fraud Prevention law, signed by Attorney General Mayes, is a rare attempt to level the playing field. It caps daily transactions at $2,000 for new customers and $10,500 for existing ones, forces operators to display bold warning screens, and requires full refunds (including fees) if fraud is reported within 30days.

Real‑World Victim Stories

Take Mary, a 68‑year‑old retiree from Peoria, Illinois. She walked up to a downtown crypto ATM, inserted $2,500 cash, and watched the screen generate a Bitcoin address. A few minutes later she received a call from someone claiming to be a “customer service rep” who asked for her private key to “confirm the transaction.” Trusting the voice, Mary shared the key, and the Bitcoin vanished instantly. The loss was irreversible, and the FBI’s data shows that cases like Mary’s are the norm, not the exception.

Scottsdale police documented a local scam where fraudsters set up a fake “exchange” booth next to a legitimate crypto ATM. They lured unsuspecting users with promises of zero‑fee trades, then stole the cash before the victim could complete the purchase.

How to Protect Yourself at the Kiosk

- Verify the machine’s operator. Look for the company name, licensing details, and a QR code that links to a verification page.

- Watch the screen for warning messages. FinCEN’s 2025 notice insists on displaying red‑flag alerts - if you don’t see them, walk away.

- Never share private keys or seed phrases. No legitimate service will ever ask for them during a transaction.

- Keep receipts. A paper receipt with the wallet address is your only proof for any refund request.

- Limit transaction size. Smaller amounts reduce exposure if something goes wrong.

- Use a hardware wallet. Transfer any purchased crypto to a personal wallet off‑line as soon as possible.

Experts like James Wyler, President of Trusted Security Solutions, stress that even a simple social‑engineering ploy can bypass sophisticated machine security. That’s why personal vigilance matters as much as technical safeguards.

Industry Response and Future Outlook

The U.S. Department of Treasury’s Financial Crimes Enforcement Network (FinCEN) issued Notice FIN‑2025‑NTC1 on August4,2025, formally warning institutions about the rising risk. It also released a set of “red‑flag indicators” to help banks flag suspicious crypto ATM activity, such as rapid high‑value purchases followed by immediate transfers to newly created wallets.

Meanwhile, AARP’s executive vice president Nancy LeaMond notes that lawmakers across the aisle are pushing for “commonsense rules that balance innovation and consumer safety.” As of 2025, 11 states have passed crypto‑ATM‑specific legislation, and 40 states introduced broader digital‑asset bills.

On the technical front, the ATM industry is eyeing the TR‑31 key‑block management standard, originally designed for traditional ATM networks. While not a cure‑all, it could tighten encryption across crypto‑ATM firmware, making exploits like CVE‑2024‑0674 harder to pull off.

Crypto ATM vs. Traditional ATM: A Quick Comparison

| Feature | Crypto ATM | Traditional ATM |

|---|---|---|

| Regulatory oversight | Minimal; many operators skip BSA/AML | Strict federal and state regulations |

| Transaction reversibility | Irreversible once blockchain confirms | Can be reversed or disputed |

| KYC requirements | Often none or basic phone verification | Mandatory ID verification |

| Typical fees | 2‑8% per transaction | Usually flat fee or free for account holders |

| Physical security | Vulnerable to firmware exploits, weak OS hardening | Hardened OS, regular audits |

Next Steps for Consumers and Operators

If you’re a user, start by checking your state’s crypto‑ATM regulations - many states now require operators to post licensing info on the machine. Keep an eye on FinCEN’s quarterly bulletins for new red‑flag updates.

For operators, the message is clear: patch firmware quickly, implement robust KYC checks, and display mandatory warning screens. Failure to comply could mean hefty fines or forced shutdowns, as Arizona’s recent enforcement actions suggest.

Finally, think of crypto ATMs as a bridge - they’re meant to make crypto accessible, not to replace the protections you get from a bank. Treat them with the same caution you’d give any high‑risk financial service.

Frequently Asked Questions

What makes crypto ATM transactions harder to recover than bank transfers?

Cryptocurrency moves on a decentralized ledger that, once confirmed, can’t be rolled back. Banks can reverse or freeze a transfer, but crypto networks have no central authority to do that.

Are all crypto ATMs unsafe?

Safety varies by operator and hardware. Machines that follow BSA rules, display FinCEN warnings, and keep firmware up‑to‑date are far less risky than unlicensed kiosks.

How can I verify if a kiosk is licensed?

Look for a license number on the screen or the machine’s body, then cross‑check it with your state’s financial regulator website. A QR code that leads to a verification page is also a good sign.

What should I do if I suspect a scam after using a crypto ATM?

Record the receipt, note the wallet address, and report the incident to local law enforcement and the FBI’s IC3. If the kiosk is in a state with a refund law (like Arizona), file a claim within the required window.

Will upcoming regulations make crypto ATMs safer?

Regulations can raise the bar for KYC, transaction limits, and operator accountability, but the core risk - the irreversible nature of blockchain transfers - will remain. Users still need to stay vigilant.

Philip Smart

October 11, 2025 AT 08:36Another crypto ATM scam story, yawn.

Jacob Moore

October 12, 2025 AT 20:43Hey folks, if you’re thinking about using a crypto ATM, double‑check the operator’s license and keep your transaction small at first. It’s the fastest way to stay safe while you get the hang of it.

gayle Smith

October 14, 2025 AT 08:50Listen up, the crypto‑ATM ecosystem is riddled with vectors of phishing and firmware exploits that cascade like a poorly‑coded smart‑contract bug. You can’t trust the shiny screen; look for the backend compliance badge before you drop cash.

mark noopa

October 15, 2025 AT 20:56We stand at the crossroads of convenience and vulnerability, where a sleek kiosk can become a portal to loss.

Every time you insert a bill, you’re dancing with a silent algorithm that holds no remorse.

The allure of instant crypto is a siren song, promising freedom while masking an invisible leash.

Remember, the blockchain is immutable; once the transaction is sealed, no bank can hit the undo button.

Those who ignore the red‑flag warnings are essentially signing a contract with the unknown.

Just as a philosopher questions the nature of reality, you must question the nature of the machine before you trust it.

Is the firmware signed, verified, and regularly patched? If not, you’re handing a key to a stranger.

Regulatory gaps are not loopholes for innovators-they’re chasms where scammers thrive.

The Lamassu vulnerabilities illustrate that even reputable vendors can slip up, leaving doors open for attackers.

In an age where KYC is optional, your personal vigilance becomes the only shield.

Keep receipts, log the kiosk’s serial number, and treat every transaction like a test run.

Transfer any purchased crypto to a hardware wallet the moment you can; offline storage is the ultimate insurance.

Never, ever, share your private key or seed phrase-no legitimate service will ask for that at the point of sale.

Finally, educate the people around you; the older demographic is especially susceptible, and community awareness can stem the tide of loss.

Stay skeptical, stay informed, and let caution be your constant companion 😎

Rama Julianto

October 17, 2025 AT 09:03Listen up, you need to demand that the ATM shows a valid state license and a clear warning screen before you even think about inserting cash. If the machine looks tampered or the firmware version is hidden, walk away-no crypto is worth that risk.

Helen Fitzgerald

October 18, 2025 AT 21:10Totally agree with the point on hardware wallets-once you pull the crypto off the kiosk, stash it in a Ledger or Trezor ASAP. It’s the fastest way to make the scammer’s job impossible.

Jon Asher

October 20, 2025 AT 09:16Good tip, Jacob. I always start with $20 to see how smooth the process is before going bigger.

Jade Hibbert

October 21, 2025 AT 21:23Wow, another genius who thinks a crypto ATM is a magic money printer. Sure, Jan, let’s trust a random box on the street with our life savings.

Leynda Jeane Erwin

October 23, 2025 AT 09:30Dear reader, while the flamboyant dramatics abound, please observe that compliance documentation, albeit a mundane formality, remains the cornerstone of operational legitimacy in this sector.

Leo McCloskey

October 24, 2025 AT 21:36Well… another ‘expert’ wades into the deep end with half‑cooked advice; readers beware!!!

arnab nath

October 26, 2025 AT 08:43They’re hiding the real agenda: it’s all about feeding the shadow network, not protecting the user.

Nathan Van Myall

October 27, 2025 AT 20:50The data shows a spike in reports after the new licensing law; it’s a clear correlation, not a coincidence.

debby martha

October 29, 2025 AT 08:56Solid summary, thanks for laying it out.

ചഞ്ചൽ അനസൂയ

October 30, 2025 AT 21:03Great point about moving assets to a hardware wallet-keeping the crypto offline is the ultimate defense.

Orlando Lucas

November 1, 2025 AT 09:10In short, crypto ATMs are a double‑edged sword: they democratize access but also expose users to unregulated risks. Stick to licensed machines, verify firmware updates, never share private keys, and keep transaction amounts low until you’re sure the kiosk is legit. The combination of regulatory oversight and personal vigilance is your best bet against becoming another statistic.

Scott Hall

November 2, 2025 AT 21:16Exactly, Orlando-keeping it simple and safe is the way to go. Thanks for the clear rundown!

Brandon Salemi

November 4, 2025 AT 09:23Bottom line: stay alert, verify, and protect your crypto.

Siddharth Murugesan

November 5, 2025 AT 21:30If you keep ignoring the obvious warnings, you’re just asking to get ripped off. Wake up.

Lena Vega

November 7, 2025 AT 09:36Thanks everyone, this thread really helped clarify the risks.